The Bertha Centre for Social Innovation and Entrepreneurship

at UCT’s Graduate School of Business is researching the applicability of Social

Impact Bonds (SIBs) to South Africa in a project that is partly funded by the

National Treasury with a specific focus on Small Business Development and job

creation. The Bertha Centre recently

held an information session with interested stakeholders in the Cape Town and

Johannesburg.

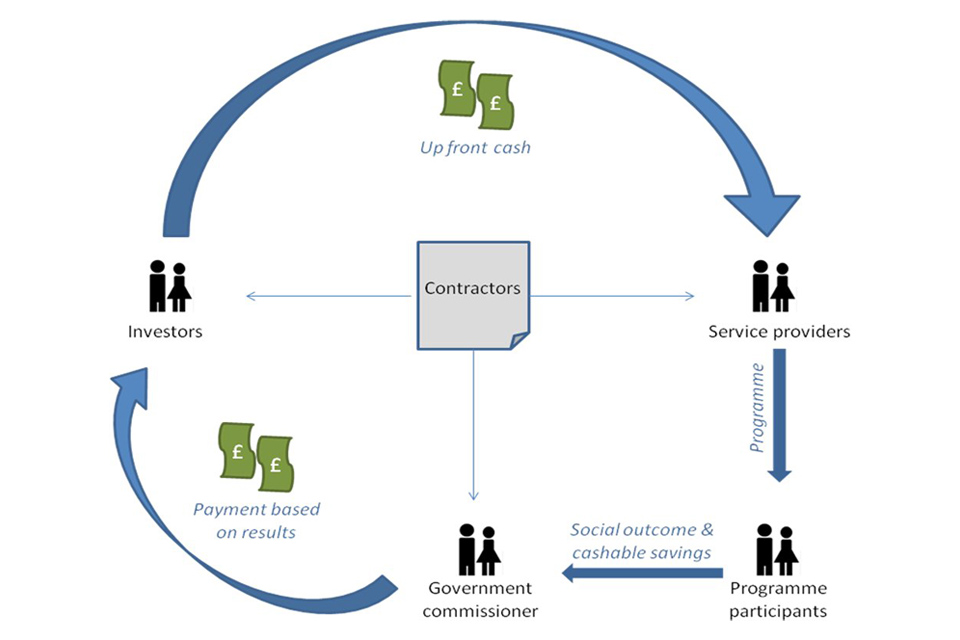

What is a Social

Impact Bond?

Image www.gov.uk

According to Ryan Short, a director of Genesis Analytics, it

is “a contract in which the government agrees to pay private investors for

securing improved social outcomes. Socially minded investors provide up-front

working capital to NGOs, charities, social enterprises and private service

providers, to fund their programmes and test innovative interventions. If the

programme achieves agreed targets, investors receive a variable return on

investment from the government — the more successful the programme, the higher

the return. If the programme fails, investors do not recover the investment.”

In short, the benefit to government and governmental

organisations is that only pays if the agreed outcome occurs and the risk of

the project transferred to the initial investor(s). It sounds pretty good for government.

Source: http://emmatomkinson.com/

as of February 2014

The first SIB was issued with much fanfare in 2010 in the

United Kingdom and was hailed as the “future in non-profit financing”. Since then 17 have been launched in the UK

and range from North America to Australia and even the Mocambique Ministry of

Health is working on one.

WHY NOT JUST GET A

REGULAR LOAN?

According to Aunnie Patton from the Bertha Centre

“In one word: incentives. In other words…

- DATA: Since outcome-based payments rely on outcomes measurement, service providers, investors and governments are incentivised to create realistic, rigorous metrics for assessing the intervention. Bonus: often this data can lead to benchmarks for similar government programmes to come.

- DILIGENCE: Government in essence outsources the due diligence of the service provider to private investors, who risk losing their capital if the provider fails (hence, again, an incentive).

- RISK: Investors are used to putting risk capital on the line for a reward commiserate with that risk. Governments are used to spending capital to provide public services. But SIBs shift the risk of a new approach, allowing governments to pay only when outcomes are delivered and investors to be rewarded for taking on the risk of the pilot (once again, incentives all around).

- COORDINATION: Often the structure of a SIB requires multiple service providers to coordinate their activities into a “total intervention”. But individual service providers are only rewarded if this total intervention works (one last time, an incentive for all).[1]”

Are these points unique to SIB’s or are we just allocating

an additional layer of administrative cost to an already overburdened

non-governmental sector meaning that even LESS money gets to the beneficiaries?

Is a SIB Necessary? Let us look at the benefits raised

above:

1.

DATA Collection –Plenty of research is already

done on the effectiveness of projects and outcomes. The Jobs Fund has discontinued significant

funding from organisations that do not reach their job creation targets per

their original contracts without a SIB in place.

2.

DILIGENCE – Here Ms Patton is correct in that

the diligence of the provider is outsourced.

It is a normal part of contracting arrangements for NGO’s.

3.

RISK – This is discussed further below, but in

essence there is very little risk being transferred.

4.

COORDINATION – This is perfectly doable in the

normal course of project funding and should be BAU.

ARE WE TRANSFERRING

RISK?

Looking through the list of investors it is telling that

there are very few new names and at least 3 of the SIB’s in the UK are funded

by the Government itself[2]

and as of June 2014 there is no mix of government and non-government funding in

UK SIB’s so the much hoped for private-public partnership does not seem to be

bearing out. In addition most of the non-governmental

funders are philanthropic organisations, organisations with a government

mandate for social investment or foundations or corporates who would be

spending the funds on similar projects as part of their sustainability

objectives. Previously these

organisations provided funding with no guarantee of return i.e. they took on

the risk. The list of parties showing interest in a South African SIB does not appear any different. Goldman Sacs appears to be an exception to the

rule, but in addition to receiving a 22% return on one of their investments

(the average return is 6-8%) they have obtained a guarantee for 75% of their

exposure to one project and are the preferred creditor in another as well in

what one article called “part of their image remake program after 2008”[3].

While there could be a transfer of risk SIB’s do not appear

to have not been effective so far in bringing new money to the problem and with

an added layer of costs (financial intermediary, administration, co-ordination),

excluding the return the effect is SIB’s are reducing the funds available to

the final recipient. It is also unlikely that private

investors are going to get involved in projects that have no track record so

the risk is related to implementation or specific circumstances rather than a

complete unknown. Is that worth the

additional cost layer? Apparently there

has been “millions of pounds worth of private funding as a result” of these

instruments according to Bertha Centre’s Dr Susan de Witt, but these numbers are not available

outside of academia and it is subjective as to whether this is additional

funding beyond “normal” social corporate responsibility levels.

The Bertha Centre is currently calling for a 30% tax relief

for social investment in addition to current donations tax exemptions and BEE

ranking benefits. In the case of a SIB

this effectively amounts to a 30% surcharge on the cost to the fiscus on a “pay

for results” investment.

There is no doubt that outcomes based project evaluation is

lacking and even basic monitoring and evaluation beyond how the funds are

spent, but the answer is not to create another layer of cost. The cost effective solution is to put

together a framework of monitoring and evaluation for all projects and ensure

that there are sufficient trained staff that this is BAU for all projects and

organisation and not just those that are lucky enough to find a 3rd

party funder willing to take the risk on them.

For a more balanced review of SIB’s in South Africa I would

recommend reading “Thinking About Social Impact Bonds in the South African

Context (lessons from the United Kingdom)[4]”

published by Cornerstone Economics which presents reasons for and against a

local SIB as well as detailed analyses of 3 of the projects in the United

Kingdom for further reading on the topic.

[2] http://emmatomkinson.com/2014/02/14/social-impact-bond-sib-uk-v-world-map/

retrieved 2014/08/14 02:00 PM

[3] http://www.reuters.com/article/2013/11/12/us-goldman-social-impact-bond-analysis-idUSBRE9AB0ZD20131112

retrieved 2014/08/07 08:32 PM

[4] http://www.cornerstonesa.net/wp-content/uploads/2014/06/Thinking-about-SIBs-in-SA-Cornerstone-Economic-Research.pdf

retrieved 2014/08/07 09:00 PM